Clear, expert-reviewed guides on funding options, policy basics, and what to expect at every stage.

How Long Does It Take to Receive Money from a Viatical Settlement?

If you are facing mounting medical bills or other financial challenges after a serious illness, you may be wondering, how long does it take to

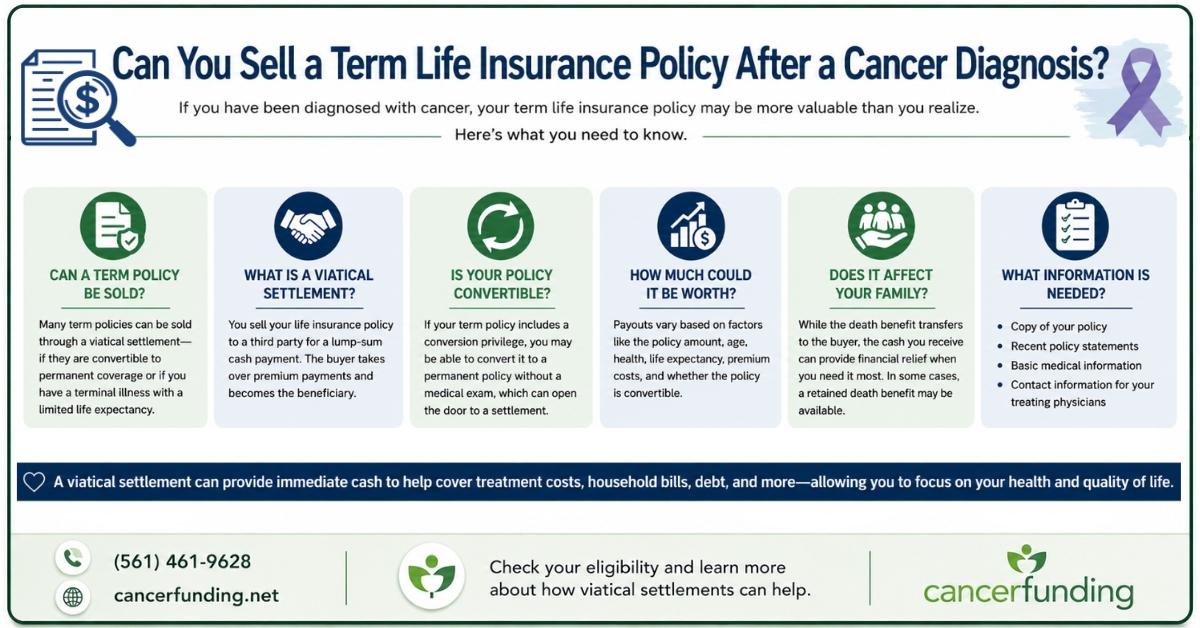

Can You Sell a Term Life Insurance Policy After a Cancer Diagnosis?

A cancer diagnosis can affect nearly every aspect of your financial life, including your life insurance coverage. If you are wondering, can you sell a

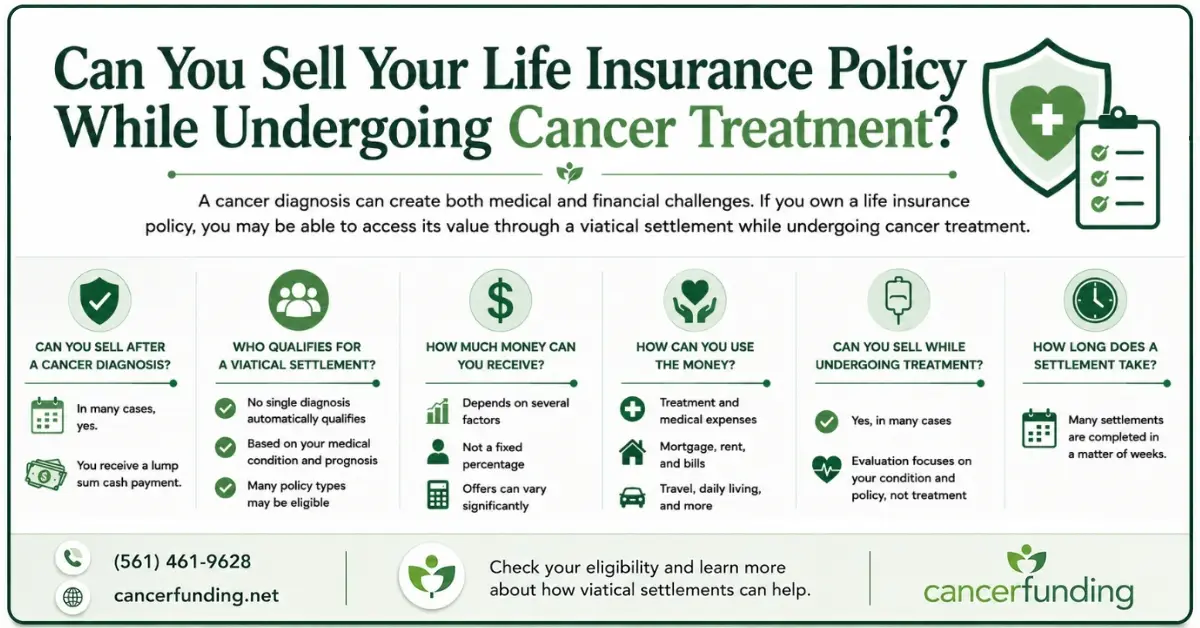

Can You Sell Your Life Insurance Policy While Undergoing Cancer Treatment?

A cancer diagnosis often brings more than medical decisions. It can also create significant financial stress, as many people search for ways to pay for